Wing A

Wing A  Wing B

Wing B  Wing C

Wing C  Ahan 2

Ahan 2 ![]()

20 March, 2023

![]()

4 mins read

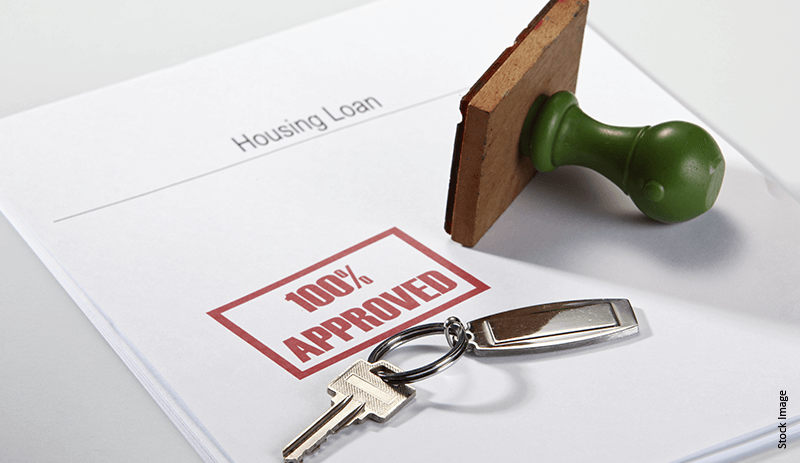

Buying a house is one of the most significant financial transactions a person makes. For some people, it is just a mode of investment to grow their wealth, whereas, for some, it is like a dream come true. No matter what, one should thoroughly evaluate their financial health before making such a big decision. If a homebuyer opts for a home loan, their responsibilities increase even more. One should thoroughly understand the home loan process before agreeing with a lender. For starters, we have covered the home loan process step by step in this article. From home loan pre-approval to loan disbursal, here’s what a homebuyer should know about the home loan procedure in India.

Home loan pre-approval is the first step of the home loan approval process. Lenders look at a homebuyer's credit score and financial status and offer pre-approved home loans. The borrower can save time, energy, and money by applying for a pre-approved home loan. They will know in advance the maximum home loan amount they are eligible for and the interest rate they will have to pay.

The second step in the home loan process is the loan application. The borrower needs to apply for a home loan with the lender of their choice. This can be done online or offline. These days, most lending institutions in India allow homebuyers to apply for a home loan online through their websites. All one has to do is fill up an online home loan application form and upload the required documents, including identity, address, and income proof. This is a simple and hassle-free process.

After receiving the home loan application from a borrower, the lender will start a home loan approval process. This is the most complex step in a home loan procedure. Generally, lenders follow the pattern mentioned below for home loan approvals:

● Determining the home loan eligibility of the homebuyer based on their age, monthly income, debt-to-income ratio, and credit score, among others.

● Verification of the documents submitted by the borrower. This may also include a field investigation to verify whether the borrower is living at their residential address.

● Legal and technical inspection of the property for which a home loan is being taken. The lender may ask for all the documents related to the property, including the the sale agreement,No Objection Certificate, Registration Certificate or Occupancy Certificate,etc

● Estimating the approximate market price of the property. Based on this estimation, the lender will decide the maximum home loan amount that can be offered.

After completing the home loan approval process, the lender will send a home loan sanction letter to the homebuyer. A sanction letter usually contains the following details:

● Maximum home loan amount a homebuyer can withdraw.

● The applicable home loan interest rate.

● The maximum tenure for which the loan can be given.

● Whether the rate of interest will be

fixed or floating.Apart from these, a home loan sanction letter can also contain the terms and conditions of the home loan. If a homebuyer agrees to these terms and conditions, they can sign the sanction letter and the formal request for the disbursal of the loan.

Once a borrower signs the sanction letter and sends it back to the lender, it starts preparing the home loan agreement. A home loan agreement contains every detail regarding the home loan, including the exact loan amount, the applicable rate of interest, payable EMI amount, date of disbursal, date of EMI, etc. A duly signed copy of this agreement will be given to the borrower, whereas the lender will keep another copy.

Finally, we have come to the last step of the home loan process, i.e., the disbursal. After receiving a duly signed copy of the home loan agreement from the borrower, the lender will start the home loan disbursal process. A borrower can decide if they want the home loan amount to be disbursed in their bank account or directly into the seller’s bank account. In the case of an under-construction property, the lender will disburse the home loan amount in instalments based on the progress of the construction.

The process of obtaining a home loan, or mortgage loan, can be lengthy and complex. Homebuyers must thoroughly understand the entire home loan process before applying. By following the six steps above and working with a reputable lender, homebuyers can confidently navigate the home loan process, avoid potential pitfalls, and make informed decisions about their financial future.

Disclaimer- This article is based on the information publicly available for general use as well as reference links mentioned herein. We do not claim any responsibility regarding the genuineness of the same. The information provided herein does not, and is not intended to, constitute legal advice; instead, it is for general informational purposes only. We expressly disclaim any liability, which may arise due to any decision taken by any person/s basis the article hereof. Readers should obtain separate advice with respect to any particular information provided herein.

![]()

![]()

![]()

![]()

![]()

13 December, 2023

![]()

05 June, 2023

One of our sales representative will be in touch with you shortly.

VIEW OUR TOWERS Table of Contents

Table of Contents